It is easy to get swept away in the maelstrom of views and counter views, but difficult to arrive at an informed decision on the subject of net neutrality -- the uninhibited access to legal online content without broadband service providers (BSPs) being allowed to block, degrade, or create fast/slow lanes to this content that rides over the internet (OTTs).

The fundamental question is why fix the internet when it is not broken and that too for the wrong reasons? These include inter alia India's overwhelming dependence on mobile broadband due to abysmal wireline penetration, coupled with scarcity and high cost of spectrum and congestion of the internet due to bandwidth hogging free riders.

To meet these challenges BSPs need tools to prevent congestion and shore up their revenues through levies on content or tie-ups with OTT providers so as to invest in infrastructure, improve service quality and make surfing affordable for the poor and bridge the digital divide. These theories demand a pinch of salt.

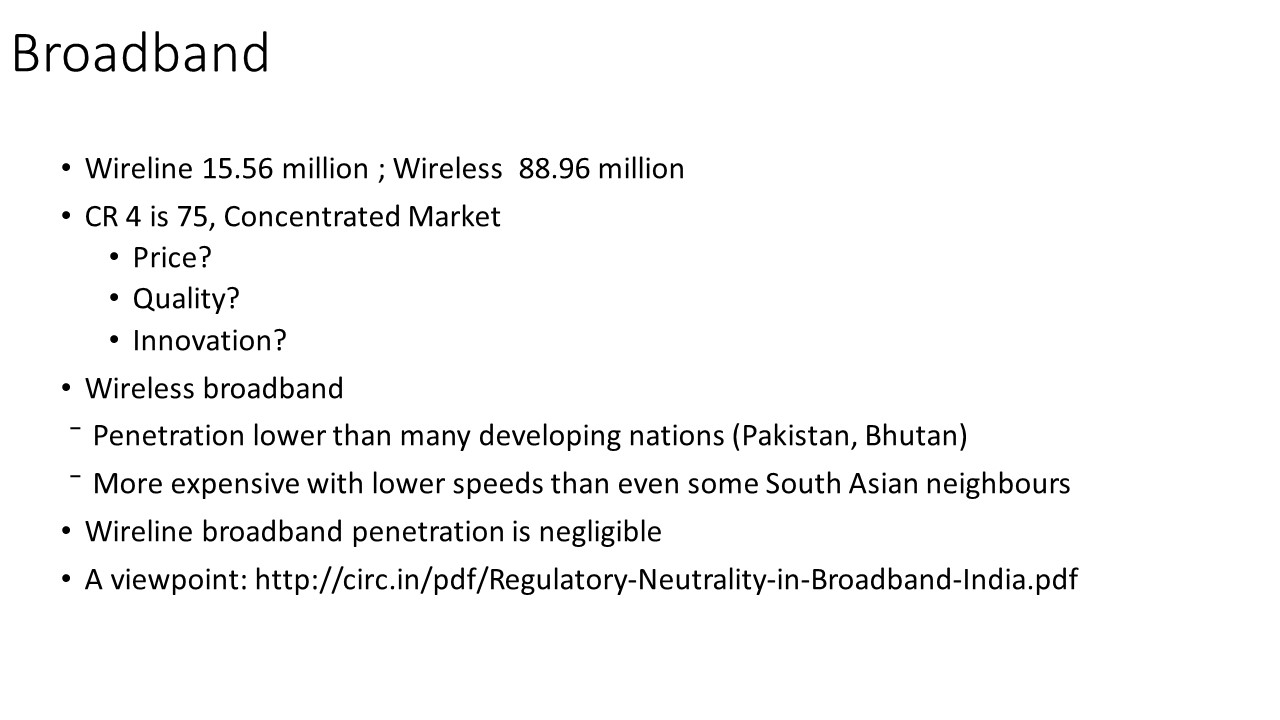

Reason One: India depends on wireless broadband. It is true that we have an abnormally high mobile to fixed broadband ratio of 4:1 and only 15.2 million wired broadband connections in a country of 1.2 billion. This has arisen from a legacy of overprotection of PSU incumbents (BSNL & MTNL) who would not allow private operators to access their infrastructure and neither was this mandated.

As PSU monopolies led to inefficiencies, but regulatory barriers made investing in wirelines unattractive, innovation driven, privately provided, wireless services took over. India has a fixed broadband penetration ratio of 1.2 per 100 as against the world average of 9.4 per 100. The incumbents continue to lose 2-3 million landline connections every year.

However, this imbalance needs to be rectified through regulatory reforms rather than accepted as permanent; nor should it become a reason for interfering with net neutrality. It's important to note also that in terms of competition and performance, we don't fare too well in the wireless broadband space either, ranking 113th in the world with a penetration ratio of 3.2 per 100, performing worse than Nepal and Sri Lanka.

We have one of the lowest broadband speeds in the world, both in wired and wireless broadband and broadband prices as a percentage of per capita incomes are higher in India than in Pakistan or Sri Lanka. The top four players command about 75 percent of the wireless broadband market. They are the new incumbents and predictably, they too would like to protect their turf.

Applications like WhatsApp and Skype represent Schumpeterian creative destruction offering much cheaper messaging and voice services over the internet. To avoid going the landline way, mobile service providers must embrace technological progress, adapt, innovate and compete, rather than being allowed to thwart consumer access to applications or OTT providers' access to consumers.

Reason two: Scarcity of spectrum. The scarcity of adequate and contiguous spectrum must be solved by better spectrum planning in the long run and the use of technology to enhance spectrum efficiency in the short run. The former includes freeing up spectrum held by defence and railways, and allowing spectrum trading and sharing.

The latter includes employing techniques like multiple small cells to support more users with the same amount of spectrum and creating Wi-Fi hot spots to shift users from mobile broadband to unlicensed Wi-Fi spectrum, whenever feasible. If additional infrastructure costs must be borne to this end or if BSPs must be incentivised to do so by rationalizing indirect taxes or through subsidies, then so be it. Meddling with net neutrality is not the right solution.

Reason three: Bandwidth hogging applications should cost more. BSPs in India offer multiple tariff plans with different browsing speeds and download limits. Beyond the download limit, the speed goes down drastically (fair usage). BSPs offer top ups, to maintain speed, albeit at a cost.

While OTT players respond by continuously innovating to make their applications more bandwidth efficient, users are certainly not enjoying a free lunch at the cost of BSPs. The more they download, the more they pay. Also, growing data usage is a source of revenue for BSPS. Data revenue has nearly doubled, from Rs.3,057.83 crore in June 2013 to Rs.5,910.28 crore in September 2014.

Reason four: BSPs need a share of OTT players' revenues to fund universal connectivity. There are more transparent and less harmful ways to encourage investment in broadband infrastructure. India has a Universal Service Obligation Fund (USOF) to subsidise and promote rural telecom services. As per USOF rules, subsidy is available to both public and private sector players and is discovered through a transparent bidding process. This makes it the ideal means to bridge the digital divide.

Reason five: Free, or cheap content to allow a taste of the internet. The utility of the internet cannot be reduced to a few applications. Notwithstanding the harm this would do by way of discouraging innovation and distorting consumer choice, do we really want our price sensitive, digitally uninformed masses' internet experience to be limited largely to Facebook or Bing?

We already rank below 11 African countries and among the Least Connected Countries on the ICT Development Index which includes ICT skills, usage and access. For deserving users, USOF can subsidise access to important applications (e-health, e-education etc.) in a transparent manner, leaving them to explore the rest of the internet as they please.

The transformative power of the World Wide Web lies in externalities created by its scale and scope - billions of users and a mindboggling array of information, products and services. Should we curb the freedom of this open exchange and that too for the wrong reasons?